For much of the past decade, the economic story was simple: money was cheap. Interest rates hovered near zero, borrowing was easy, and even mediocre business plans could look viable when financing costs were negligible. That era is over — and it may not be coming back soon.

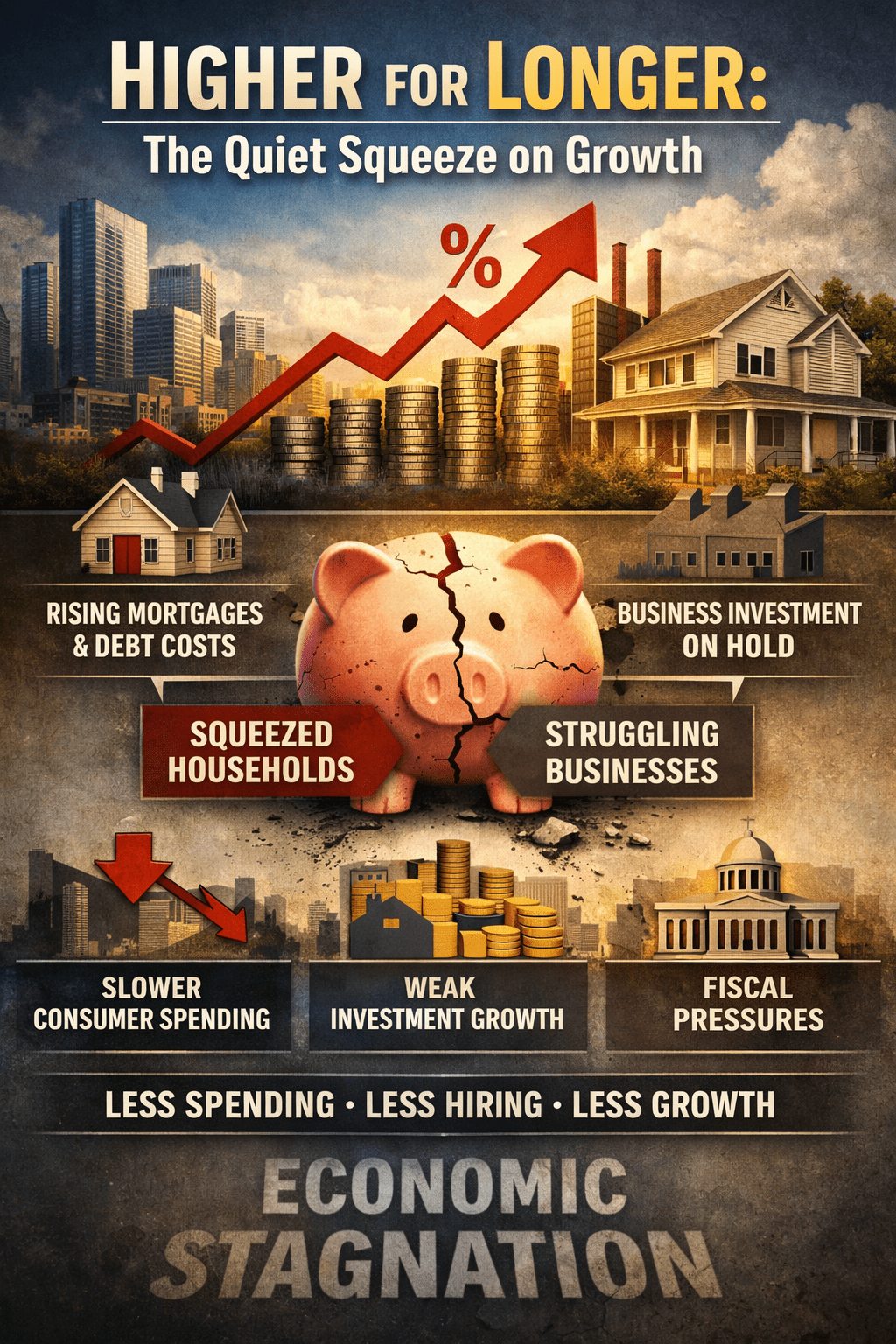

“Higher for longer” has become the defining phrase of the current cycle: central banks keeping interest rates elevated for an extended period to ensure inflation is truly under control. It sounds technical, even boring. But its consequences are anything but. Quietly, persistently, higher rates squeeze growth across the economy — not through a single dramatic crash, but through thousands of smaller decisions that add up to slower spending, weaker investment, and a more cautious business environment.

Why rates are staying high

The basic logic is straightforward. When inflation rises, central banks raise interest rates to cool demand. Higher rates make borrowing more expensive, which tends to reduce consumer spending and business investment. That lower demand then eases price pressures.

The complication is that inflation isn’t just a one-off spike. It can become sticky — embedded in wage negotiations, services pricing, rents, and expectations. Central banks know that cutting rates too early risks reigniting inflation, which would force another round of tightening later. So even as inflation falls from its peak, policymakers may keep rates high until they’re confident the job is done.

The result is a world where interest rates aren’t “temporarily high” but structurally more normal — closer to historical averages than the ultra-low post-2008 period.

The household squeeze: less room to spend

For households, the impact is immediate and personal. Mortgage payments rise for those on variable rates or refinancing fixed deals. Credit card debt becomes more expensive. Car finance costs climb. Even those who don’t borrow feel the pinch indirectly: landlords facing higher mortgage costs often pass them on through higher rents, and businesses facing higher costs may raise prices where they can.

When a larger share of income goes to servicing debt and essential bills, discretionary spending falls. People delay renovations, skip big purchases, and cut back on non-essentials. That might sound like common sense, but macro economically it matters because consumer spending is a major engine of growth.

The “quiet” part of the squeeze is that it doesn’t always show up as a sudden collapse. Instead, it appears as a gradual flattening: fewer restaurant meals, slower retail sales, less travel, more households choosing to save “just in case”. The economy doesn’t crash — it just loses momentum.

Businesses feel it in the balance sheet

If households are squeezed through monthly payments, businesses are squeezed through financing conditions. Companies that relied on cheap credit now face higher interest costs when they roll over debt. Firms that planned to expand may reconsider, because the hurdle rate — the return required to justify an investment — has risen.

This matters most for small and medium-sized enterprises (SMEs), which typically have less access to cheap capital markets and rely more heavily on bank lending. A large firm might issue bonds, hedge interest-rate exposure, or draw on cash reserves. A small business often can’t. Higher rates don’t just make expansion harder; they can make survival more fragile.

Even healthy firms may shift behaviour. Instead of investing in new equipment, training, or hiring, they focus on protecting margins and maintaining cash flow. That is rational at the company level — but at the economy level, it leads to weaker productivity growth, which ultimately limits wage growth and living standards.

The investment drought becomes a growth problem

Higher rates act like gravity on investment. Property development slows because financing costs and risk increase. Venture capital becomes more selective because safe assets (like government bonds) offer better returns than they did when rates were near zero. That makes funding scarcer for start-ups and more expensive for scaling firms.

In the long run, this is one of the biggest dangers of “higher for longer”: it doesn’t just cool demand today, it can reduce the economy’s productive capacity tomorrow. Underinvestment means fewer productivity improvements, slower innovation, and weaker future growth.

This is especially concerning for economies already struggling with productivity — where growth relies heavily on investment in skills, infrastructure, and technology. If high rates discourage that investment, the economy can become trapped in a low-growth equilibrium: not collapsing, but not thriving either.

Winners exist — but they don’t drive growth

It’s important to say: not everyone loses in a higher-rate world. Savers earn better returns on deposits and bonds. Some pension funds benefit from improved yields. Banks may enjoy stronger net interest margins (at least initially). People with little debt can even feel more financially secure.

But these “winners” don’t necessarily translate into stronger growth. Higher interest income often goes to households more likely to save than spend. Meanwhile, the groups cutting back are often those with mortgages, consumer debt, or tight budgets — the very people whose spending fuels the everyday economy.

So even when higher rates create pockets of benefit, the overall effect can still be a drag on demand.

Government finances: less room to manoeuvre

Governments aren’t immune either. Higher interest rates increase the cost of servicing public debt, especially as bonds mature and are refinanced at higher yields. That can crowd out spending on public services or force politically difficult tax rises.

At the same time, weak growth reduces tax revenues. So the state faces a double pressure: higher financing costs and a softer economy. That makes fiscal policy more constrained just when public investment might be most needed to support long-term growth.

What to watch next

The key question isn’t whether rates will fall eventually — they likely will, at some point. The real issue is the path: how quickly, how far, and whether inflation stays under control.

Three indicators matter most:

- Wage growth: If wages rise too quickly, inflation can remain sticky.

- Services inflation: Often harder to bring down than goods inflation.

- Business investment: A leading signal of future productivity and growth.

If those remain elevated or fragile, central banks will hesitate to cut. And if they do cut, they may do so slowly.

The bottom line

“Higher for longer” isn’t a headline-grabbing crisis. It’s a slow, structural shift that changes behaviour across the economy. Households spend less, businesses invest less, governments have less flexibility, and growth weakens through a thousand quiet compromises.

The danger isn’t a dramatic collapse. It’s stagnation: an economy that keeps moving, but not fast enough to improve living standards in a meaningful way.

In that sense, higher rates don’t just cool inflation — they reshape the entire growth story.

Bank for International Settlements (BIS) — Annual Economic Report 2023 (June 2023).